white

I recently went through open enrollment at my company, and felt fully confident beforehand that I would contribute mightily to a DCFSA (Dependent Care Flexible Spending Account). Well, I was wrong. I ended up not opting for any DCFSA payroll deductions, and here’s why:

It’s more complicated than it sounds.

Sadly you can’t use these funds to pay for your local babysitter, or cover the Venmo payment you send the nanny every week. In order to use DCFSA funds, you need to make sure that you’re following the good ol’ IRS guidelines.

This blog post will focus on those guidelines, and other questions you’re surely asking yourself about the DCFSA benefit.

All us parents would certainly rejoice if we could just pay the nanny straight from our DCFSA account, but it’s not that simple. You can technically use DCFSA funds to pay a nanny or a neighborhood babysitter, but the fact of the matter is that you can’t do it "under the table."

To get reimbursed, the IRS requires you to provide the Taxpayer Identification Number (TIN) or Social Security Number (SSN) of the care provider on Form 2441 when you file your taxes. Yep, like I said–compicated.

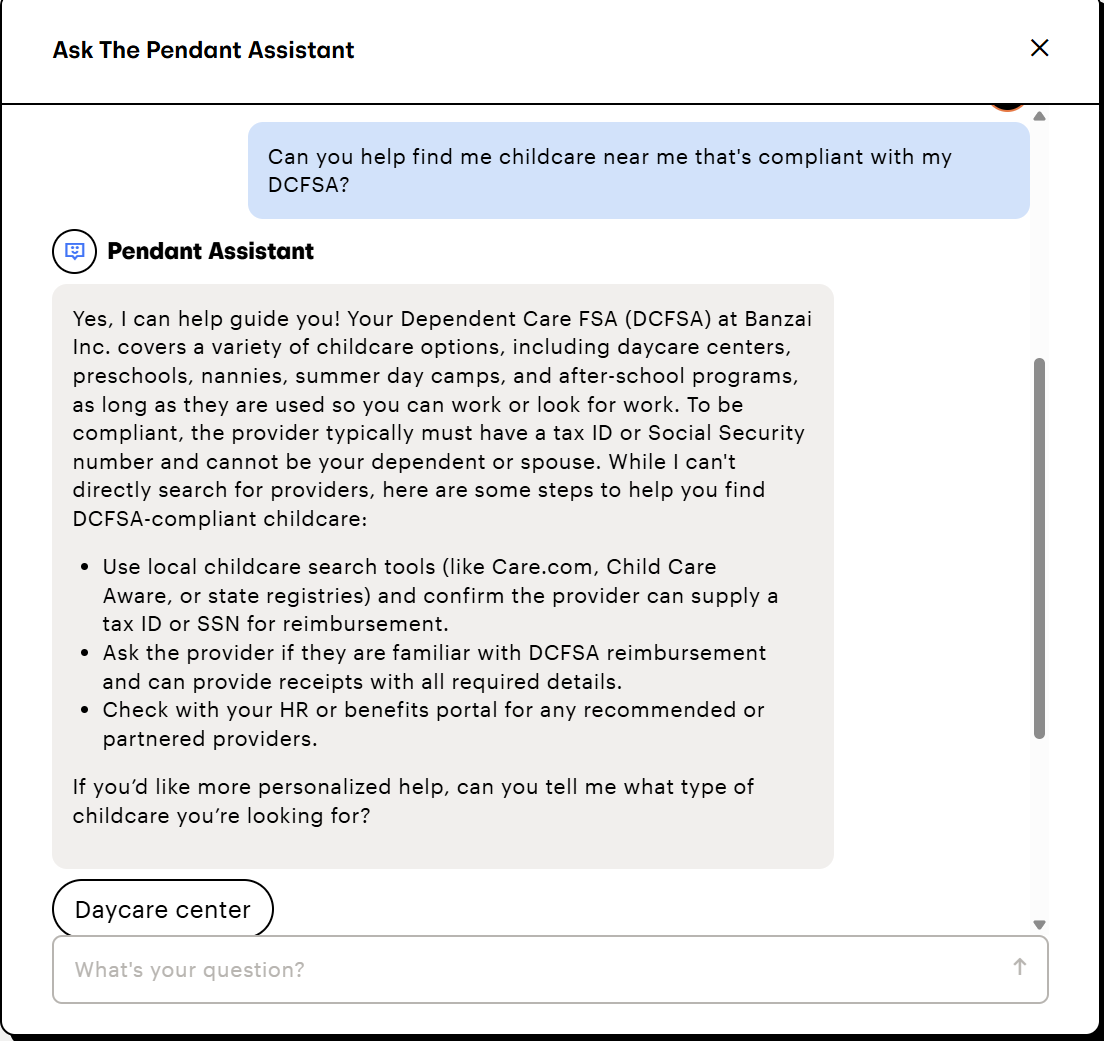

When it comes to complicated things like this, my first stop is always the Pendant A.I. Assistant. Here’s how my conversation went:

Well, this seems like an excellent place to start! While it’s true that paying my mother-in-law, or my niece with my DCFSA account isn’t a possibility, you can still find a caregiver that checks off all the necessary boxes.

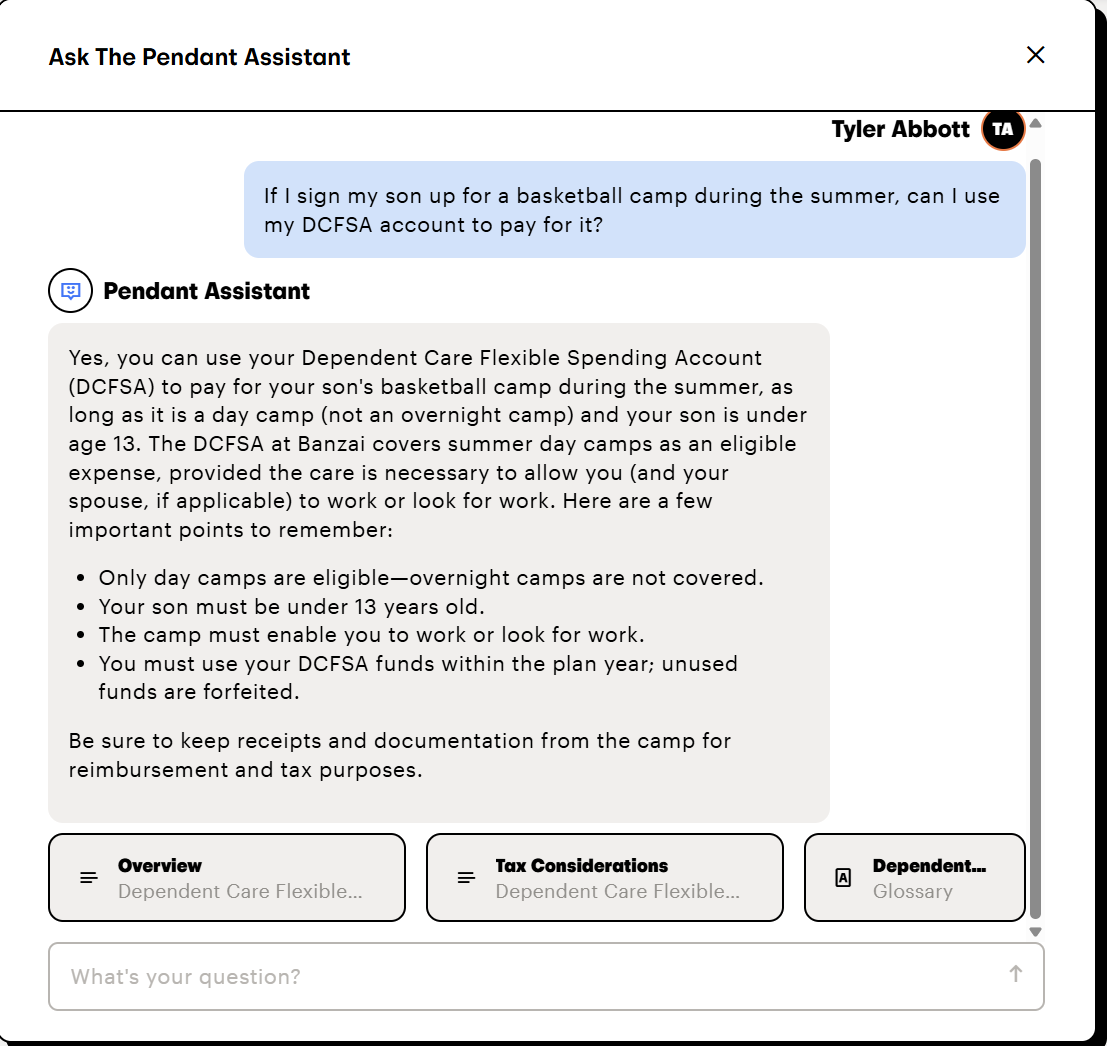

If you are anything like me, you probably see the word "camp" and think "Oh yeah, that’s childcare." But it turns out the IRS is a little more particular (shocker!). While summer day camps generally get the green light—since they technically function as care during work hours—overnight camps are a different story. The IRS views those 24-hour sleepaway camps as "recreational" rather than necessary work-related care, which means you unfortunately can't use your DCFSA funds to cover them.

Here’s what the Pendant AI Assistant had to say:

Well, shoot. I’m starting to realize using a DCFSA account is easier than I thought. Darn it. Now I’m having enrollment regret all over again.

In case we haven’t hammered it enough, you can only use DCFSA funds for childcare if you’re performing one of these three activities:

This means you technically cannot use your DCFSA balance to pay a caregiver to catch a movie or run errands on your day off.

Here’s another tricky one–The IRS considers nursery school and preschool as eligible DCFSA expenses, but not Kindergarten.

As soon as your child enters Kindergarten, the switch flips and the IRS views it as "education," rather than childcare. The silver lining? You can still use your DCFSA funds for your kindergartener’s before- or after-school programs.

If you are unsure where that line is drawn, you can always just ask the Pendant AI Assistant for any particular preschools or after-school programs.

At the beginning of this blog post I felt pretty convinced that a DCFSA wouldn’t make sense for my family. I have a six-year-old son who began Kindergarten this year and a 16-month daughter that won’t start preschool for a while, so I thought I wouldn’t need a DCFSA until next year. Turns out the DCFSA coverage goes wider than I thought. Well, there’s always next year.